Understanding Home Addition and Depreciation: What You Need to Know

When it comes to managing a rental property, making additions or improvements is a common practice to increase its value and extend its useful life. However, it's essential to understand how these changes affect the property's depreciation. Home addition and depreciation are intricately connected, and failing to grasp this concept can lead to incorrect tax calculations, penalties, and missed opportunities for deductions.

What Constitutes Home Addition and Depreciation?

Home additions and improvements are permanent changes to a property that enhance its value, increase its useful life, or adapt it to new uses. Examples of such additions or improvements include building a new room, replacing the roof, remodeling, installing new plumbing or wiring, or adding fences. These changes are subject to depreciation, which is an essential aspect of real estate tax calculations.

Why Do Home Additions and Improvements Have an Impact on Depreciation?

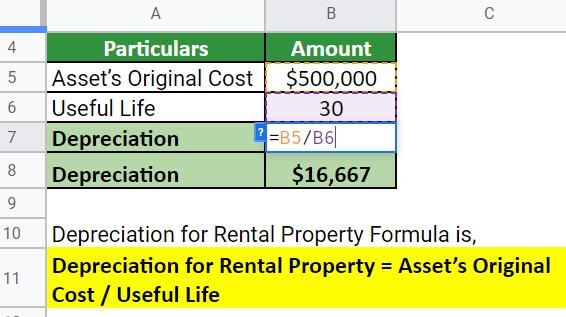

Depreciation is the gradual decline in value of assets over time, and home additions and improvements are considered assets that require depreciation. When you create a new room or renovate an existing space, the cost of these changes gets added to the property's basis. This means that the property's value is adjusted to reflect the new additions or improvements. As a result, the property's useful life is extended, and its value increases, thus requiring depreciation to account for the asset's wear and tear.

How to Depreciate Home Additions and Improvements

When depreciating home additions and improvements, you need to consider the following:

- Separate Properties: For situations where additions or improvements are made to separate properties, each property should be depreciated separately.

- Modified Accelerated Cost Recovery System (MACRS): MACRS is a depreciation method that allows for accelerated depreciation of certain assets. The MACRS class for an addition or improvement is generally determined by the MACRS class of the property to which the addition or improvement is made.

- Depreciation Period: The period for figuring depreciation begins on the date that the addition or improvement was placed in service and will be determined by the MACRS class.

- Eligibility: To qualify for depreciation, an item needs to be placed in service during the tax year or within 60 days of the end of the tax year. Additionally, it should not be rent or lease back to the taxpayer in the tax year or in any of the following 8 tax years.

Examples of Home Improvements and Depreciation

Here are a few examples to illustrate the concept of home addition and depreciation:

- Adding a room to a rental property for business use: The cost of the new room will be depreciated over a 39-year period using the straight-line method of depreciation.

- Replacing the roof on a rental property: The new roof will be depreciated over a 27.5-year period using the straight-line method of depreciation.

- Installing new plumbing or wiring: These improvements will also be depreciated over the life of the property, typically 27.5 years for residential rental property.

Conclusion

Understanding home addition and depreciation is crucial for rental property owners. Misunderstanding this concept can lead to incorrect tax calculations, penalties, or lost deductions. By grasping the basics of depreciation, you can leverage your real estate investment to its fullest potential and maximize tax benefits. Always consult a tax professional or financial advisor for personalized guidance on home addition and depreciation.

, How To Depreciate Property")

- Internal Revenue Service")